Stepping through the new negative gearing and CGT method statements

TaxEverything you knew about using negatively geared losses and calculating capital gains or losses is changing.

This article is the first in a two-part series explaining the changes to negative gearing and CGT and how the new rules will operate in practice.

All legislative references are to the Income Tax Assessment Act 1997 (Cth) (ITAA 1997).

The negative gearing and CGT measures in the federal budget 2026–27 are now law, given effect by the Treasury Laws Amendment (Tax Reform No. 1) Act 2026 (Cth) (Budget Act). Much of the commentary has focused on what is being taken away: the 50 per cent discount and the ability to deduct negatively geared rental losses against other assessable income. Less attention has been paid to the machinery that replaces them.

From 1 July 2027, three new method statements will govern the numbers, and ordering the losses incorrectly will produce the wrong tax outcome.

The three core changes to the ITAA 1997 are:

-

The loss quarantining rules (Schedule 2 to the Budget Act), in new sections 26-155 and 26-160.

-

The CGT rewrite (Schedule 1 to the budget Act), positioned primarily in new Subdivision 112-E, and a recast of the CGT method statement in section 102-5.

-

The new minimum 30 per cent tax, a separate regime again, in new Division 119.

The three method statements are interrelated, and the connections are where the complexity lives.

New terminology

Four new categories of capital gains have been created to enable the quarantining of negatively geared losses from residential property. Capital gains must also be apportioned between those accruing before 1 July 2027 (deferred capital gains) and those accruing from that date.

From 2027–28, a capital gain must be identified as:

-

A deferred residential capital gain (DRCG)

-

A deferred non-residential capital gain (DNRCG)

-

A residential capital gain (RCG)

-

A non-residential capital gain (NRCG)

Quarantining negatively geared losses

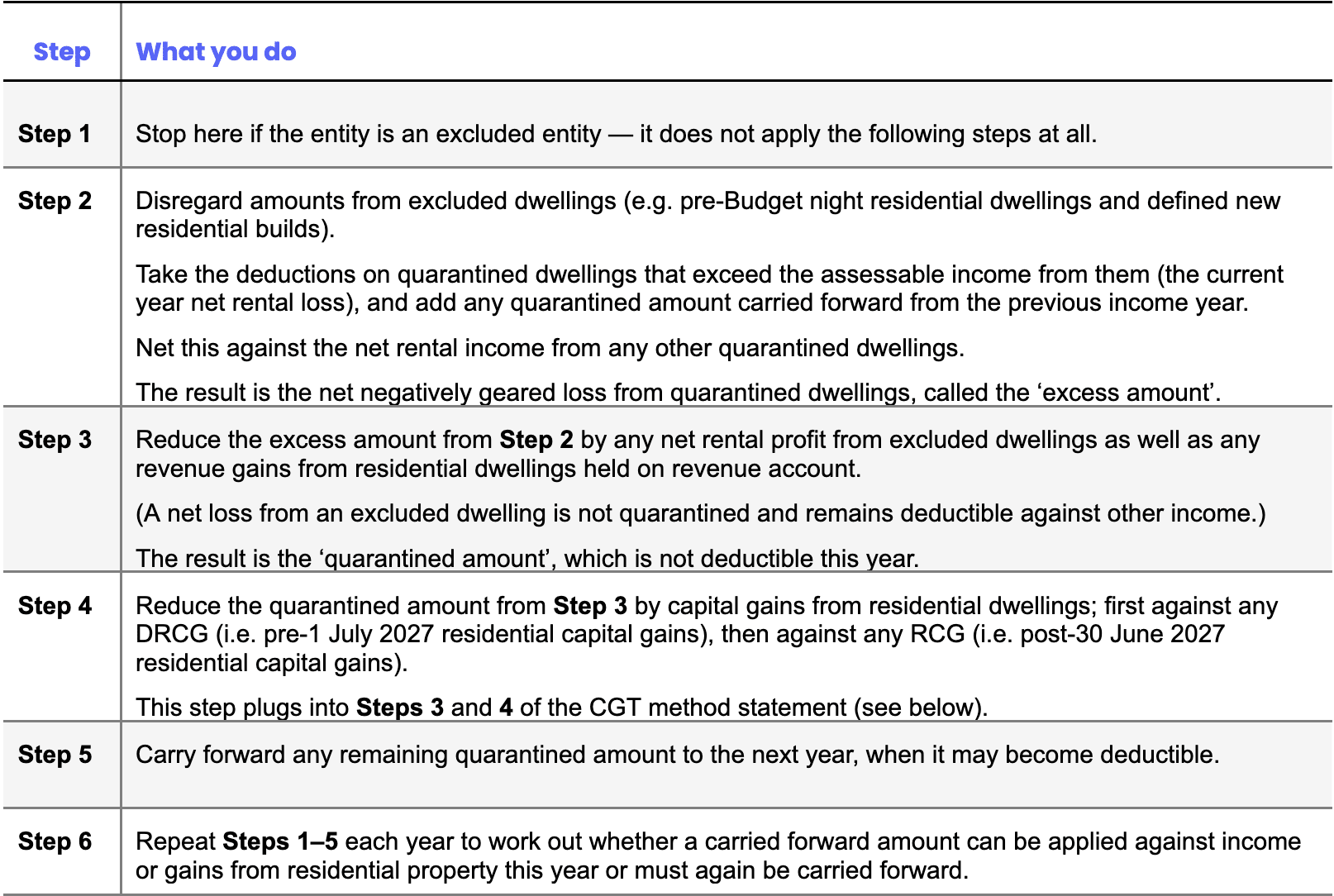

From 1 July 2027, a net rental loss on an established residential dwelling acquired at or after 7:30 pm AEST on 12 May 2026 (budget night) can no longer be deducted against salary, business or other non-rental income in the year it arises. The losses are not lost; they are quarantined (set aside and carried forward) unless offset against net rental income or gains from residential property.

The six-step method statement below determines each year how much of the loss is quarantined, how much can be used, and how much is carried forward.

Three points frame the exercise:

-

Quarantining is worked out at the portfolio level, not property by property, so a loss on a quarantined dwelling can be netted against income from another residential dwelling;

-

Excluded dwellings – residential dwellings (including vacant land) acquired before budget night and certain defined new builds are not subject to the rules; and

-

Excluded entities – widely held trusts (such as managed investment trusts) and complying superannuation entities (including self-managed superannuation funds) sit outside the rules entirely.

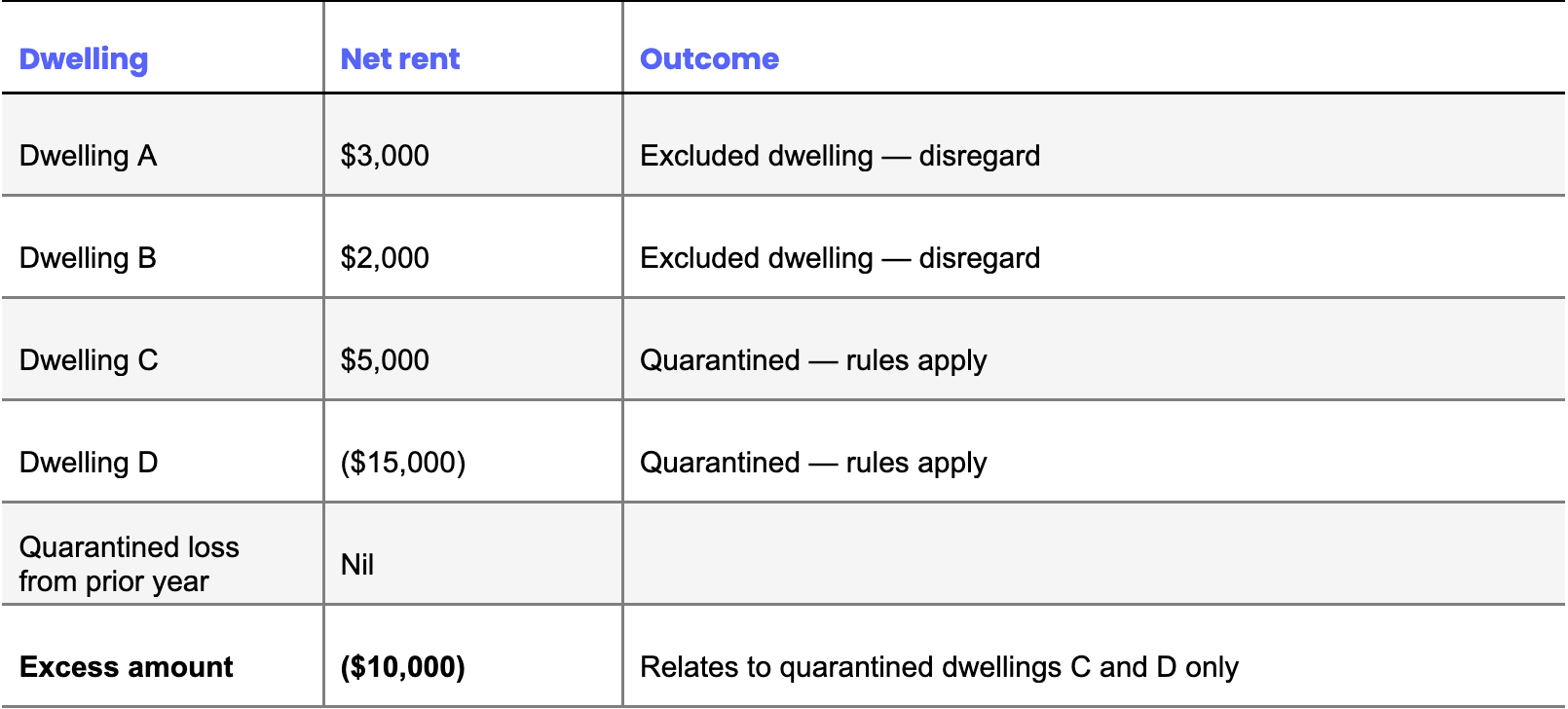

Worked example 1

(Based on example 2.5 from the explanatory memorandum to the enabling legislation)

Tyson acquired established dwellings A and B in 2025 (excluded dwellings) and established dwellings C and D after budget night (subject to quarantining). He considers 2027–28 first.

2027–28

Step 1

Tyson is not an excluded entity, so the steps apply.

Step 2

Tyson works out the net rent from each property and the excess amount:

Step 3

The net rent from excluded dwellings A and B of $5,000, less the excess amount of $10,000 for dwellings C and D, leaves a quarantined amount of $5,000. This is not deductible in 2027–28.

Step 4

Tyson has no residential capital gains in 2027–28, so there is nothing to apply the quarantined amount against (it would go first to any DRCG, then any RCG).

Step 5

The $5,000 quarantined amount is carried forward to 2028–29.

Step 6

Tyson repeats steps 1-5 in 2028–29 (see below).

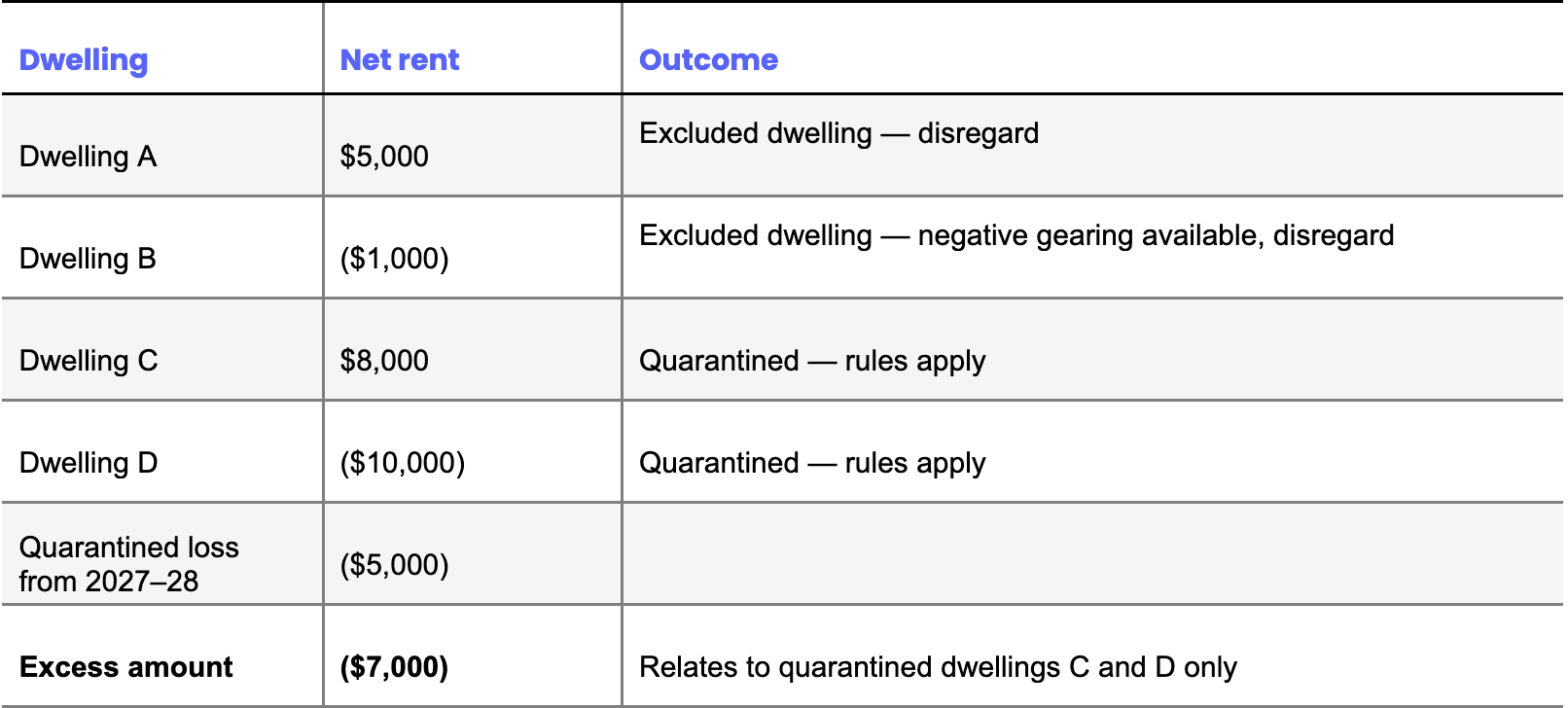

2028–29

In 2028–29, the $5,000 carried-forward loss is treated as relating to a residential dwelling. Tyson disposes of dwelling B, making a $20,000 capital gain.

Step 1

Tyson is not an excluded entity.

Step 2

The net rent and excess amount are:

Step 3

The net rent from A and B of $4,000, less the excess amount of $7,000 for C and D, leaves a quarantined amount of $3,000. This amount is not deductible in 2028–29.

Step 4

Tyson applies the $3,000 quarantined amount against his $20,000 residential capital gain, reducing it to $17,000. (The example does not specify whether the gain is a DRCG or RCG, but it is reduced either way.)

Step 5

No quarantined amount remains to be carried forward to 2029–30.

Nothing was permanently lost, but the deductions were deferred – in this case, by one year.

Applying capital losses: the new CGT method statement

For CGT events on or after 1 July 2027, the 50 per cent discount is replaced by cost base indexation, and the freedom to choose which capital gains to apply capital losses against is removed.

A mandatory seven-step method statement in subsection 102-5(1) now dictates the order. The sequence matters because losses must be applied to the deferred categories first, and those are the gains that may still carry the 50 per cent discount.

The ordering rule can halve the value of a capital loss

Under the current rules, a taxpayer may apply capital losses against non-discount gains first, preserving the discount on the gains that qualify. That choice is gone from 1 July 2027; capital losses must be applied against the deferred categories first (which may still be eligible for the discount), so a capital loss delivers only half its value.

Worked example 2

Assume that in 2026–27 a taxpayer has an $800,000 gain on an asset held for less than 12 months (no discount), a $500,000 discount gain, and a $200,000 carried forward capital loss.

Under the current rules, the taxpayer applies the capital loss against the $800,000 non-discounted gain (reducing it to $600,000) and applies the discount to the $500,000 gain (reducing it to $250,000), resulting in a net capital gain of $850,000.

On the same facts, but with the CGT event instead happening in August 2027, the new ordering rule requires the capital loss to be applied against the $500,000 deferred gain first (reducing it to $300,000). The discount then applies (reducing it further to $150,000), and the $800,000 is added, leaving a net capital gain of $950,000.

The $100,000 difference is half the loss amount. From 1 July 2027, some capital losses will be worth only half what they are today.

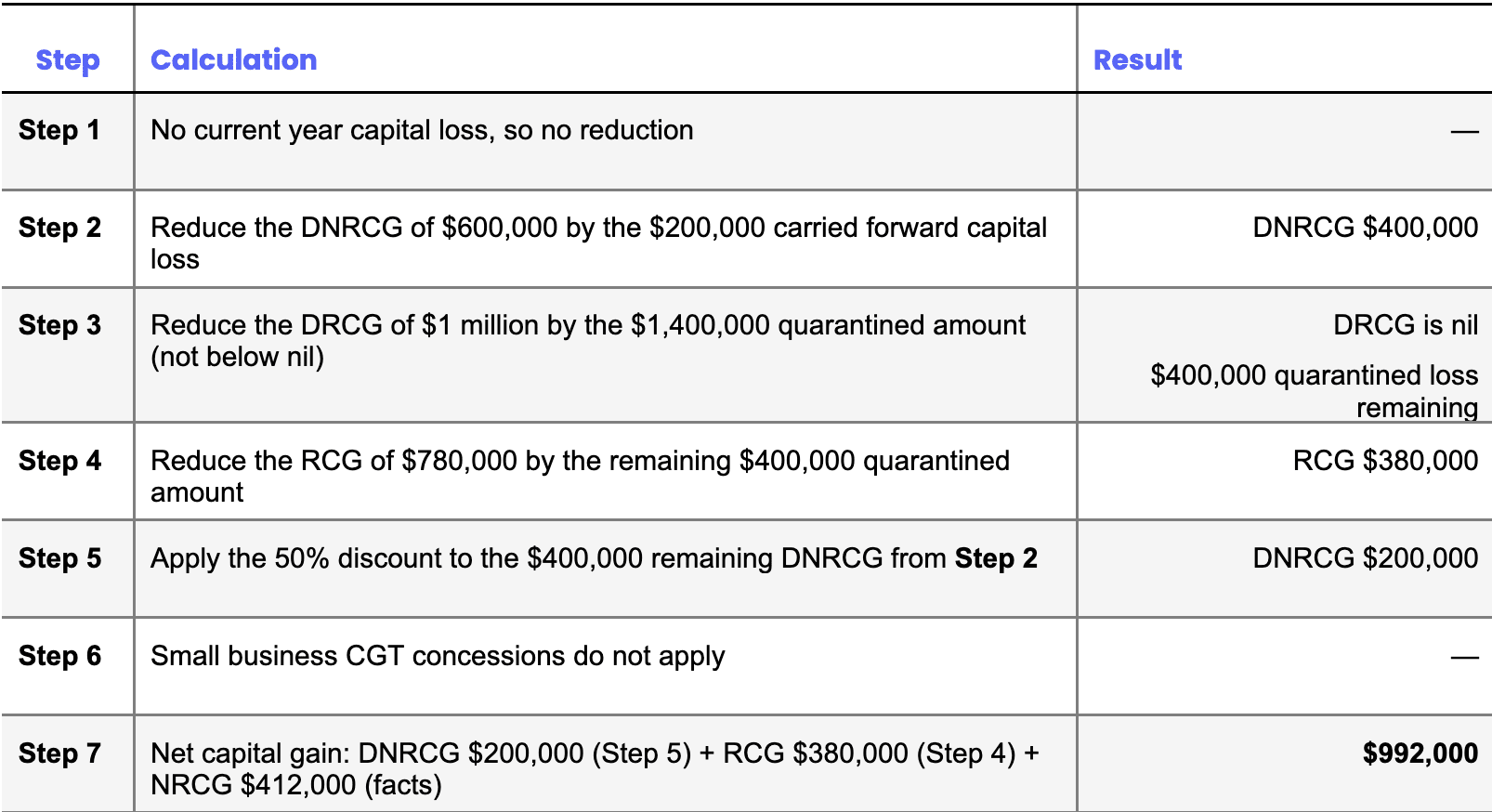

Worked example 3

(Based on example 1.9 from the explanatory memorandum to the enabling legislation)

Asher, an Australian resident, sells four investments in 2030–31, classifying his gains as: DNRCG $600,000, DRCG $1 million, NRCG $412,000 and RCG $780,000.

He also has a $200,000 carried-forward capital loss and a $1,400,000 negatively geared quarantined amount, and is not eligible for the small business CGT concessions.

Applying the method statement:

Two features stand out:

-

The carried forward capital loss is forced against the discounted DNRCG first (Step 2), even though a taxpayer may prefer to shelter a non-discounted post-1 July 2027 gain; and

-

The negatively geared quarantine amount is fully utilised as it wipes out the DRCG entirely and then spills over to reduce the RCG (Steps 3 and 4).

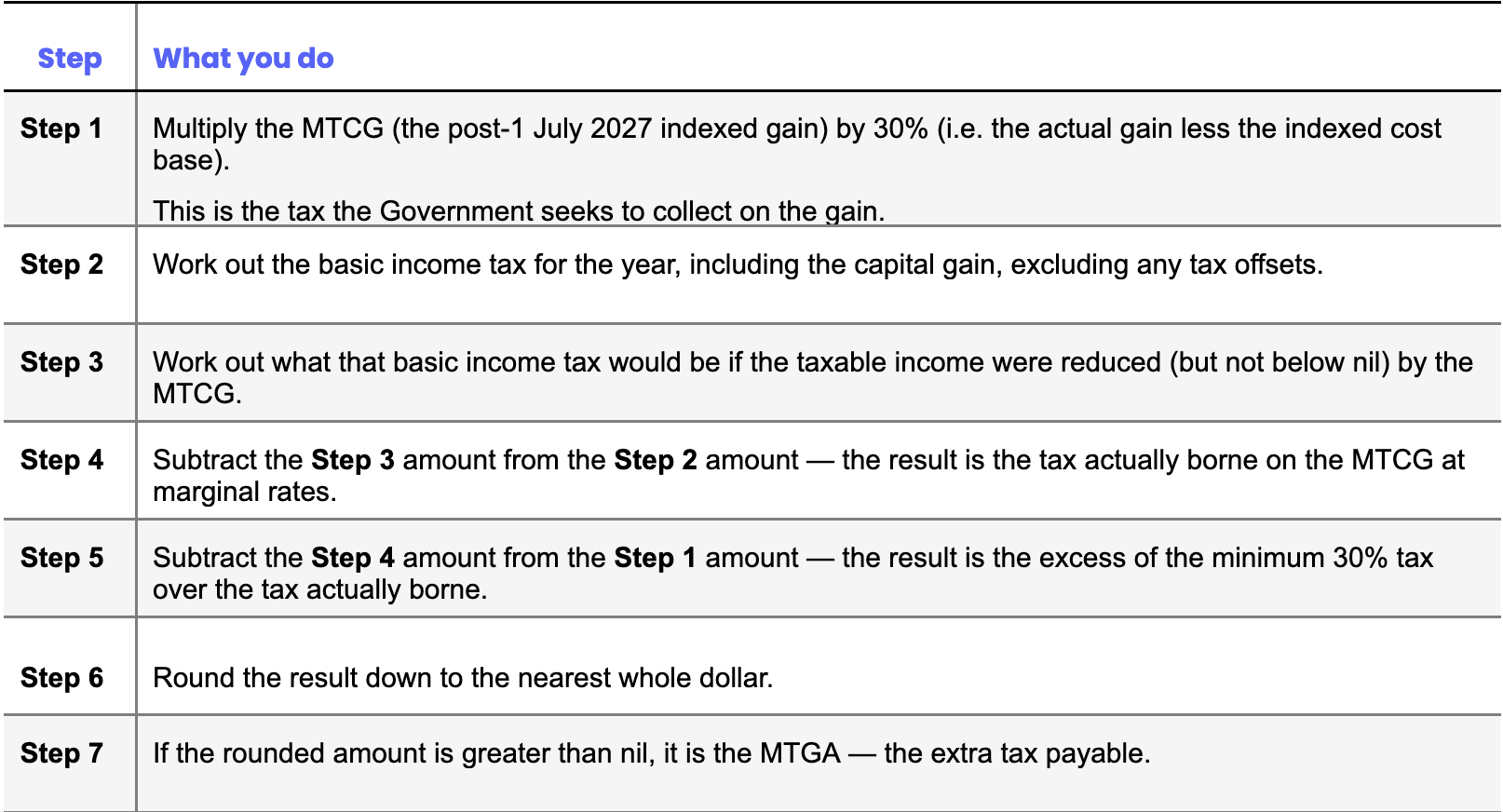

Calculating the minimum 30 per cent tax on capital gains

The third method statement calculates the minimum 30 per cent tax in new Division 119 (with the rate set by the Income Tax Rates Amendment (Tax Reform No. 1) Act 2026 (Cth)). The 30 per cent rate is a minimum rate, not a flat rate.

It applies only to the minimum tax capital gain (MTCG) – the post-1 July 2027, indexed portion of a gain – and tops up the tax on that portion only where the taxpayer’s effective rate on it is below 30%. A taxpayer already paying 30 per cent or more on the gain pays no top-up tax.

It applies to Australian resident individuals (and individual beneficiaries entitled to a trust gain), but not to gains on new residential dwellings or affordable housing (unless the taxpayer chooses indexation plus the minimum tax). Recipients of certain government payments, including the age pension, disability support pension, parental leave pay and JobSeeker, are carved out.

The MTCG is first reduced by deductible gifts under Divisions 30 and 31.

The method statement below calculates the minimum tax gap amount (MTGA).

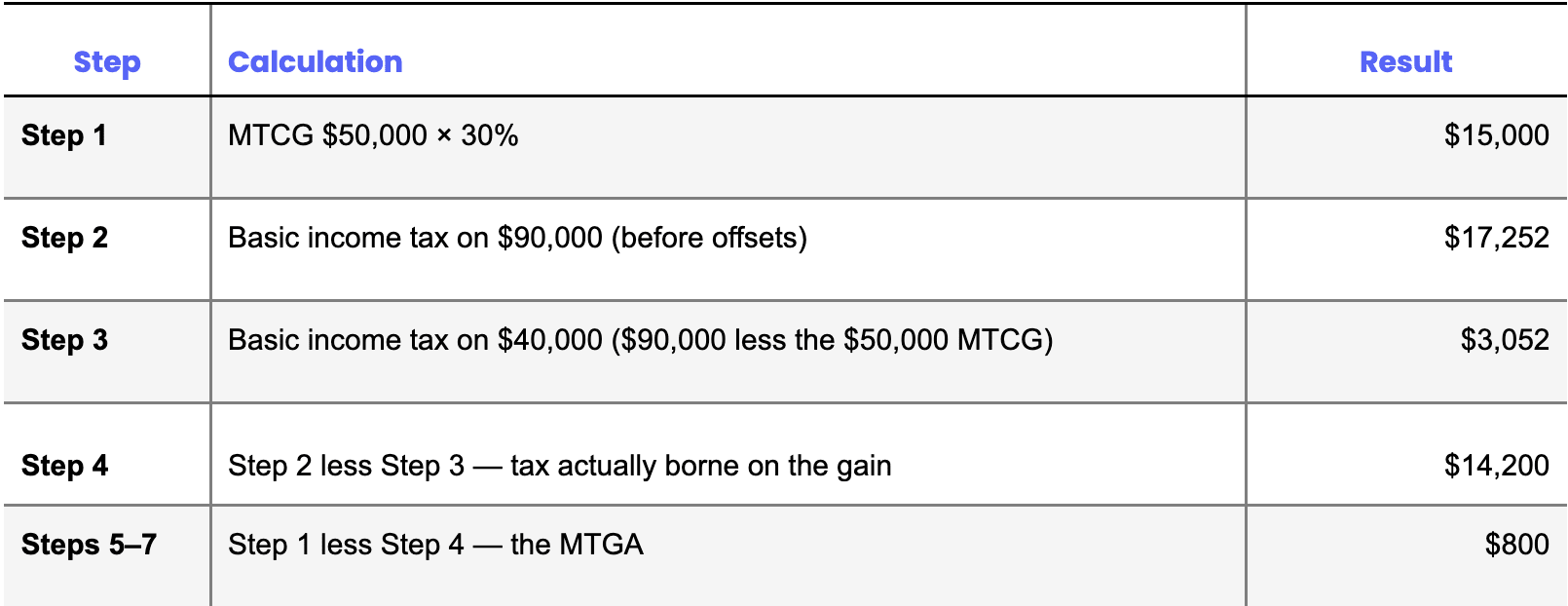

Worked example 4 – a lower-income earner

(Based on example 1.17 from the explanatory memorandum to the enabling legislation)

Genevieve sells listed shares in 2028–29, producing an MTCG of $50,000. Her other taxable income is $40,000, so her total taxable income is $90,000. She receives no government payments.

(The figures use the personal tax rates legislated to apply from 1 July 2027.)

There is a trap worth flagging to clients: deductions against ordinary income, such as personal concessional contributions or negatively geared losses, reduce the tax borne on the gain at step 4, which increases the MTGA at step 5. Deductions that lower a client’s ordinary income tax can therefore push up the minimum tax on their capital gains. The interaction is not intuitive and should be modelled rather than assumed.

The minimum tax also cannot be calculated until the client’s taxable income for the year is finalised, because it depends on the basic income tax borne on that income, disregarding the new tax.

What this means in practice

Each method statement is complex in isolation; the complexity rises sharply once they interact. The negatively geared quarantined amount computed under the loss method statement feeds directly into steps 3 and 4 of the CGT method statement. The mandatory loss ordering can halve the value of a capital loss. And the minimum 30 per cent tax sits on top, calculated only on the indexed post-1 July 2027 slice of the gain, and sensitive to deductions claimed elsewhere in the return.

All of this is before the new indexation and apportionment rules for pre- and post-1 July 2027 gains are layered on, and before the changes to the taxation of trust income, which are even more complicated.

For practitioners, the message is to start modelling now, on real client facts, before the 1 July 2027 commencement. The rules we knew so well, for clients with capital gains, negatively geared residential property portfolios, and carried forward capital losses, must be relearned, and fast.

In part two of this series, I examine some of the nuances of the new rules.

About the Author

Robyn Jacobson is the senior advocate at the National Tax & Accountants’ Association Ltd (NTAA). She is a fellow of NTAA, CA ANZ, and CPA Australia, and a chartered tax adviser with The Tax Institute.

About NTAA

NTAA is a prominent not-for-profit association, established in 1992 to support tax agents, accountants and tax advisers. For more than 30 years, NTAA has advocated on behalf of its members and supported them through its highly regarded tax seminars, products and hotline service. NTAA is a major representative voice for the tax community, representing more than 45,000 practitioners.

Read more at ntaa.com.au

Make Accountants Daily a preferred news source on Google.