No safe distance: the call your clients are about to make

BusinessHow accountants can lead through geopolitical disruption.

Parts one and two mapped the problem. Part one showed how the Middle East conflict transmits into Australian business costs through energy and freight, imported inflation, and currency pressure. Part two mapped where that exposure lands hardest across your client portfolio: construction, hospitality, agriculture, retail, and transport. This final piece is about what you do with that map.

The call is already coming.

It is a Wednesday morning. A client you have not spoken to since their last quarterly review rings your direct line. They skip the pleasantries. Their fuel surcharge invoices have risen by 30 per cent in six weeks. Their biggest supplier just notified them of a price review effective next month. Their bank called yesterday to discuss covenant headroom. They want to know what to do.

This call is not hypothetical. It is already happening for some practitioners. For others, it is weeks away. The question is not whether your clients will reach this moment; it is whether you are ready to be useful when they do.

Research consistently shows that SME owners contact their accountant before their banker or their lawyer when facing financial stress. Not their financial adviser. Not their industry association. Their accountant. That reflects a depth of trust unmatched by any other professional relationship in the SME ecosystem. It also creates a specific obligation: when the call comes, the conversation cannot start from scratch.

The practitioner who arrives at that call with a framework, a clear read on the client’s specific exposure, and three concrete actions already prepared is worth 10 times the one who says they will look into it. The difference is not expertise; it is preparation. And preparation starts now, before the escalation, not after.

Human-led AI, not AI-led humans, and in this context, that means the accountant leading the conversation with judgement and preparation, not waiting for the client to set the agenda.

The gap between what clients need and what most practices offer

There is a structural tension in how most Australian accounting practices are positioned right now. The compliance function, tax returns, BAS, financial statements, and audit are reliable, credentialed, and in demand. The advisory function, scenario planning, strategic risk, and business continuity are valued by clients, yet they are delivered inconsistently.

This gap is well documented. The CPA Australia and Chartered Accountants ANZ research on practice evolution has consistently shown that SME clients rate proactive advisory contact among their highest priorities, while practitioners consistently underestimate how often clients want that contact. The discrepancy is not malicious; it is structural. Most practice management systems are built around compliance calendars rather than client risk events. When a geopolitical shock creates a client risk event, the system does not flag it. The client feels alone with a problem they cannot fully articulate.

A Middle East escalation is precisely the kind of event that exposes this gap. It is not reflected in a tax deadline or a reporting period. It arrives sideways, through freight invoices, nd fuel bills and softening forward orders. And it arrives for multiple clients simultaneously, which means the practice with a prepared framework can serve 10 clients efficiently, while the practice starting from scratch for each one is quickly overwhelmed.

The firms that permanently close this gap are the ones that emerge from this period with stronger client relationships and clearer positioning as strategic advisors. The ones that do not close it will handle the compliance work competently and wonder why clients feel less loyal than they used to.

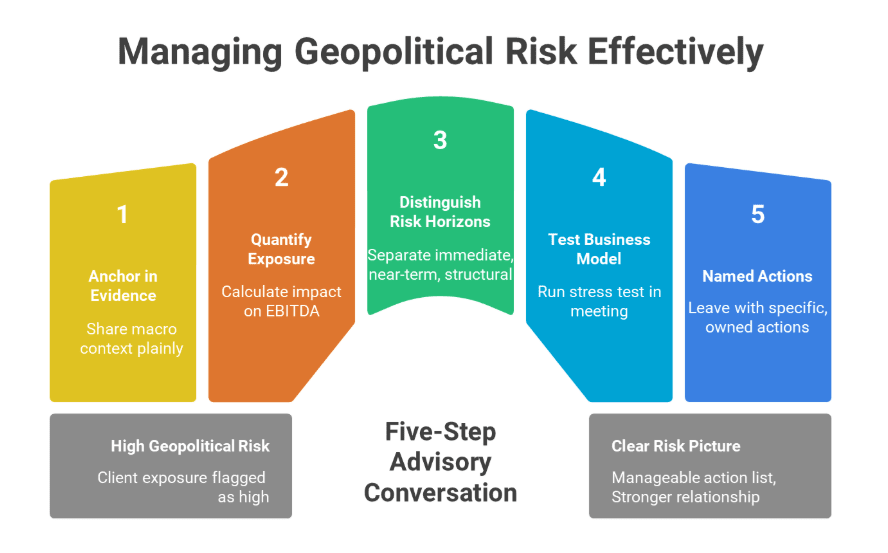

The five-step geopolitical risk advisory conversation

This is the framework I use to structure the advisory conversation with any client whose exposure the Five-Factor Scan from part two has flagged as high. It is designed to be completed in a single 45-minute meeting, with clear outputs at each step.

Step 1, Anchor the conversation in evidence, not alarm

Begin by sharing the macro context in plain language: the Red Sea disruption, the freight cost trajectory documented by the Reserve Bank, the oil price sensitivity tied to Iranian tensions, and the AUD currency exposure.

Clients respond badly to vague warnings. They respond well to specific data. The RBA’s February 2026 Statement on Monetary Policy flagged that a Middle East escalation represents an active upside risk to Australian inflation, that is, a credible, authoritative source. Use it. Frame the conversation as: “Here is what the Reserve Bank is watching, here is how it connects to your business, and here is what we are going to do about it.” This immediately elevates the conversation above speculation.

Step 2: Quantify the specific exposure

Do not generalise. Before the meeting, pull the client’s expenditure on fuel, freight, and imported goods for the past 12 months from their accounts. Calculate what a 15 per cent and 25 per cent increase in those line items does to their EBITDA. If they have fixed-price supply contracts, identify when those contracts expire and what repricing risk sits at renewal. If their customers are concentrated in the exposed sectors identified in part two, estimate what a 10 per cent reduction in revenue from those customers would do to their cash position.

Arrive with numbers, not impressions. The client’s job is to make decisions. Your job is to make those decisions possible.

Step 3: Distinguish immediate, near-term, and structural risk

Not everything needs to be solved today. Help the client separate the three horizons.

-

The immediate risk, fuel and freight cost increases already in the pipeline, requires an adjustment to cash flow now.

-

The near-term risk, potential further escalation driving oil above ninety US dollars per barrel, or a Strait of Hormuz incident disrupting energy markets, requires scenario planning and contingency preparation.

-

The structural risk, the possibility that global supply chains are permanently more fragile than before 2020, requires a strategic conversation about supplier diversification and business model resilience that may take 12 to 18 months to address properly.

Conflating all three creates paralysis. Separating them creates a workable action plan.

Step 4: Test the business model under stress

Ask the client a single question they will find uncomfortable: if your three most volatile cost lines increase by 20 per cent and remain at that level for nine months, does this business remain viable?

The RBA’s February 2026 Statement noted business debt has grown strongly, returning to near pre-pandemic levels as a share of GDP. A client who has drawn on credit facilities to fund recent expansion is running with less buffer than their current P&L suggests. The going concern assessment is not just an audit obligation; it is the most useful analytical service you can provide right now.

Run the stress test in the meeting, not later. The client needs to see the answer while you are in the room.

Step 5: Leave with three named actions and an owner for each

Every advisory conversation that ends with a vague commitment to “keep an eye on things” has failed. Leave the meeting with three specific, named actions: who does what, by when, and what the trigger is for the next conversation. These actions should be drawn from the three deliverables described in the next section.

The client’s confidence in their accountant rises in direct proportion to the specificity of the guidance they receive. Vague is not prudent. Vague is unhelpful.

Every client who goes through this conversation with a prepared adviser emerges with a clearer picture of their risk, a manageable action list, and a significantly stronger sense of who their most valuable professional relationship is.

Three deliverables you can produce right now

These are the tangible outputs that translate the advisory conversation into client value. Each can be produced within the existing scope of most accounting engagements. None requires specialist geopolitical expertise, only the willingness to connect available financial data to the risk context established in this series.

Deliverable 1: The scenario-based cash flow model. Build a 12-month rolling cash flow model with three scenarios: base case (current cost assumptions), stress case (fifteen per cent increase in fuel, freight, and imported goods costs), and severe case (twenty-five per cent increase).

The model does not need to be sophisticated; it needs to be specific to the client’s actual cost structure. The purpose is not to predict what will happen; it is to show the client what their cash position looks like under plausible conditions, so they can make decisions now rather than when the numbers are already deteriorating. For clients with seasonal revenue patterns or high fixed-cost structures, this model is the single most useful thing you can produce in the next thirty days.

Deliverable 2: The supply chain cost sensitivity analysis. Map the client’s top 10 input costs by dollar value and identify which are exposed to freight, energy, or imported goods pricing.

For each exposed item, calculate the cost impact of a 10, 15, and 20 per cent price increase. Then overlay the client’s pricing power: for each input category, can they pass the cost through to customers, and in what time frame? This analysis does two things. First, it identifies the one or two cost lines where the exposure is most concentrated, which is rarely where clients assume it is. Second, it gives the client a negotiating brief for supplier conversations, which is far more productive than anxious monitoring.

Deliverable 3: The contingency trigger document. This is the most underused tool in the SME advisory toolkit. A contingency trigger document identifies in advance the specific conditions that would require a predetermined response.

For example, if fuel costs rise above a defined threshold, the business activates a fuel surcharge clause with customers. If a major supplier announces price increases above a certain percentage, the business initiates a dual-sourcing conversation with an alternative supplier. If forward orders fall below a defined level for two consecutive months, the business reduces variable staffing to protect cash. The document does not require the triggers to be met; its value lies in removing the decision-making burden during a moment of stress. When the trigger is hit, the response is already agreed upon. That is the difference between a business that responds to disruption and one that reacts to it.

Governance as enabler, not blocker, and right now, that means giving clients the governance tools to navigate disruption before they are inside it, not after.

The myth that will leave clients exposed

Myth:

“This situation will stabilise in the next few months. We should wait and see before making any significant changes.”

Reality:

This is the most costly advice a practitioner can give, not because escalation is certain, but because the cost of waiting is asymmetric. If the conflict stabilises, a client who has built a cash flow model, reviewed their supply chain costs, and prepared a contingency document has lost a few hours of advisory time. If the conflict escalates, if oil moves above $90, if a Strait of Hormuz incident disrupts energy markets, if the Australian dollar falls sharply on a risk-off event, a client without those tools is making decisions under pressure with incomplete information.

The RBA’s February 2026 Statement explicitly identified Middle East escalation as an active upside risk to the Australian inflation outlook, in an environment where the cash rate is already at 3.85 per cent, and underlying inflation is running at 3.4 per cent. The Reserve Bank is not “waiting to see.” Neither should your clients. The three deliverables above take less time to produce than the average quarterly review. There is no credible argument for delay.

What this series has really been about

Three articles. One argument: the Middle East conflict is not a remote event with tangential relevance to Australian SMEs. It is an economic weather system that has been forming for two years, is already affecting freight costs, energy pricing, and consumer sentiment, and carries escalation risk that the Reserve Bank is actively monitoring.

The industry risk map in Part Two identified where the exposure is concentrated. The advisory framework in this article identified how to act on it. The three deliverables give you concrete tasks to produce for every at-risk client over the next 30 days.

But the deeper argument is about the accountant’s role. The compliance function will always be necessary. The advisory function determines whether a client survives a disruption with their business intact and whether they attribute that survival to the quality of their professional relationships.

The Middle East conflict will eventually resolve. The question it has raised about the accountant's role will not. The practices that answer it now, by being prepared, proactive, and specific, will hold a different kind of relationship with their clients on the other side of this.

Andrew Cooke is the founder of Growth & Profit Solutions AI (GPS-AI), specialising in helping Australian businesses navigate AI transformation and strategic risk.

Sources: Reserve Bank of Australia, Statement on Monetary Policy, February 2026; Reserve Bank of Australia Bulletin, “How Do Changes in Global Shipping Costs Affect Australian Inflation?”, July 2025; CPA Australia, “The Future of the Accounting Profession”, 2024; Chartered Accountants ANZ, “SME Advisory Research”, 2024.

Make Accountants Daily a preferred news source on Google.