No safe distance: the shockwave you can’t see yet

BusinessHere’s how the Middle East is reshaping the Australian economy, writes Andrew Cooke.

The phone call came on a Tuesday morning in late January.

A family-owned, third-generation building materials supplier in Brisbane, with 12 employees, had just received a freight invoice for a container of engineered timber fittings sourced from a European supplier. The cost was 38 per cent higher than the previous order placed six months earlier. No explanation accompanied the invoice. The owner's first instinct was to ring their freight forwarder. Their second, within the hour, was to ring their accountant.

That instinct was right. The explanation had nothing to do with their supplier or their forwarder. It had everything to do with a conflict 10,000 kilometres away.

Distance is not insulation

Australia is a long way from the Middle East. That geographic fact creates a comfortable illusion: that what happens in the Red Sea, the Strait of Hormuz, or across the Iran-Israel fault line stays there.

It doesn't. And the evidence is accumulating quickly.

The Reserve Bank of Australia's February 2026 Statement on Monetary Policy notes directly that while geopolitical tensions have so far had limited direct economic effect, an escalation in the Middle East "could raise oil prices, which would increase inflation and weigh on activity globally." That is the RBA, a cautious institution by any measure, explicitly flagging the Middle East as an active upside risk to the Australian inflation outlook. They are not doing that as a footnote. They are doing it while simultaneously raising the cash rate to 3.85 per cent and projecting underlying inflation to peak at 3.7 per cent in mid-2026.

We are not watching this from a safe distance. We are already living with its early effects, and most of our clients don't know it yet.

The conflict that began in October 2023, now in its third year, has expanded well beyond its initial theatre. Iran-aligned proxy forces, including Houthi operatives in Yemen, have sustained attacks on commercial shipping in the Red Sea. Hezbollah activity across Lebanon has driven periodic escalation. The Strait of Hormuz, through which roughly 20 per cent of the world's seaborne oil supply transits each year, remains a pressure point that financial markets have not yet fully priced. And Iran's direct military posture has shifted in ways that would have been unthinkable three years ago.

This is what I think of as a slow-moving economic weather system. It formed in the region. It has been tracking outward. And it is arriving on Australian shores in ways that are easy to miss, precisely because the connection is not obvious, until the freight invoice arrives.

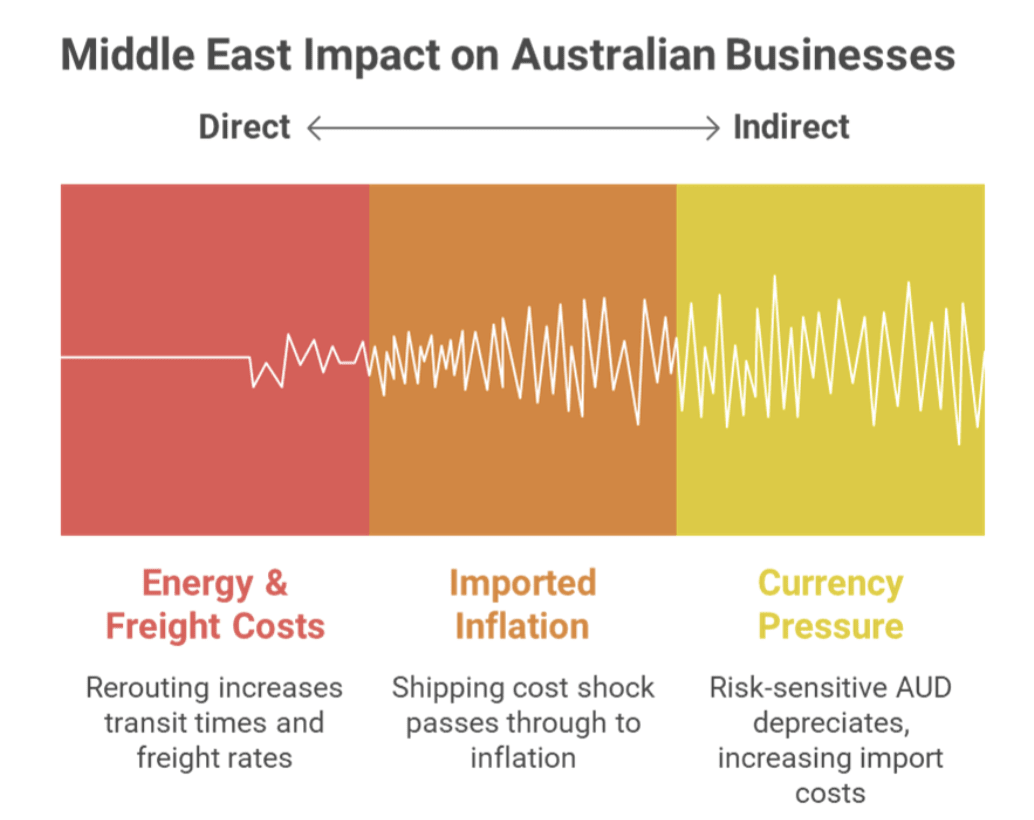

3 channels your clients are exposed to

Understanding how distant conflict reaches domestic balance sheets requires precision about the transmission mechanism. There are three channels that matter most to Australian businesses and to the accountants advising them.

Energy and freight costs

The first is energy and freight costs. Around 15 per cent of global maritime trade normally transits the Suez Canal each year, according to analysis published in the Reserve Bank's July 2025 Bulletin. Since the onset of Houthi attacks on commercial shipping in late 2023, vessels have been forced to reroute via the Cape of Good Hope, adding approximately 30 per cent to transit times and reducing effective global shipping capacity by around 5 per cent. The downstream effect on freight rates was severe: container rates reached nearly four times their 2019 average at the peak of the disruption through 2024, with the China Containerised Freight Index rising up to 75 per cent in year-ended terms during that period.

Australia is directly in the path of this. China is our largest source of imports, which is precisely why the RBA uses China-origin freight benchmarks as its primary measure of shipping cost exposure. When those rates spike, our importers pay more. When importers pay more, they either absorb the cost or pass it through. In most cases, they pass it through.

Imported inflation

The second channel is imported inflation and the RBA's constrained capacity to respond. The Reserve Bank's research found that approximately 75 per cent of a global shipping cost shock passes through to Australian freight services inflation within two quarters. That is faster than most firms expect, and the effect persists for up to 18 months. For goods that actually arrive by ship, what the RBA defines as "shippable" goods, representing roughly 25 per cent of the consumer price basket, a 10-percentage point shock to global shipping costs translates to roughly 0.4 percentage points of additional inflation after one year, and up to 0.75 percentage points after two years.

That matters acutely in the current environment because Australia's inflation trajectory was already strained before any further escalation. The RBA raised the cash rate to 3.85 per cent in February 2026, with underlying inflation running at 3.4 per cent, well above the 2–3 per cent target band. Any freight or energy cost shock from a Middle East escalation lands on a fire that is not yet out. The RBA cannot simply cut rates to cushion the impact. That is the trap. It is also the context that most SME advisers are not yet helping their clients understand.

Currency pressure

The third channel is currency pressure. The Australian dollar is a risk-sensitive currency. When global sentiment turns defensive, as it does when geopolitical risk escalates, international investors move capital into perceived safe havens: US Treasuries, gold, and the Japanese yen. The AUD depreciates. A weaker Australian dollar immediately increases the cost of all imported goods priced in foreign currencies, from electronics to pharmaceuticals to auto components. The February 2026 RBA Statement observed that gold and other precious metals prices have continued to rise rapidly, a quiet but reliable signal that institutional investors are already hedging against exactly this kind of risk scenario.

These three channels do not operate independently. They compound. A Middle East escalation that lifts oil prices, disrupts Suez Canal transit, and triggers a risk-off currency event simultaneously hits an Australian SME through higher fuel and freight costs on imported goods, and a weaker dollar that makes everything more expensive. The business owner who called their accountant in Brisbane was experiencing the leading edge of this system.

The myth that will cost firms dearly

Myth:

"The Middle East conflict has been going on for two years; if it was going to significantly affect us, we'd know by now."

Reality:

This logic confuses the absence of a visible crisis with the absence of exposure. The conflict has operated at a sustained simmer, generating persistent friction in freight markets and energy prices rather than a single dramatic shock. The RBA's own research demonstrates that shipping cost impacts on Australian consumer prices take six to 12 months to fully manifest, meaning the effects of 2024's freight rate surge are still working through the supply chain. More importantly, the escalation risk has not diminished; it has increased.

Heightened tensions involving Iran's direct military posture, its influence over the Strait of Hormuz, and ongoing proxy force operations represent a qualitative shift in regional stability. Firms waiting to see a "significant" impact before acting may wait until the damage is already embedded in their cost structure.

The 3-channel exposure audit

I use this framework when I need to give a client a rapid but rigorous first-pass assessment of their geopolitical exposure. It is not exhaustive. It is designed to be completed in a single conversation, with the output being a clear sense of where the risk is concentrated and what the immediate priorities are.

Channel 1: Energy cost exposure:

What proportion of the client's direct costs are fuel or energy-denominated?

For transport businesses, hospitality operators, and agricultural firms, this is typically their most volatile cost line. An escalation that drives Brent crude back above US$90 per barrel, plausible if the Strait of Hormuz faces sustained disruption, given its role in global oil supply, would add directly to fleet running costs, heating and cooling costs, and agricultural machinery costs. Currently (16 March), it sits at US$103.99. The task here is to quantify the dollar exposure, not estimate it. Ask the client to pull their fuel and energy spend for the last 12 months. Then model a 15 per cent and a 25 per cent increase. The number matters more than the scenario.

Channel 2: Import and supply chain dependency:

How much of the client's cost structure depends on imported goods or materials?

The question is not simply whether they import, but whether their suppliers import, and whether those imports transit affected shipping routes. A retailer sourcing from a domestic distributor may not realise that the distributor sources from European or South Asian manufacturers whose goods cross the Suez Canal. Map the supply chain two steps deep, not one. The freight bill for the Brisbane timber supplier arrived from a European vendor, but the actual exposure was a Red Sea rerouting that the client had no visibility over until the invoice landed.

Channel three: Pricing power and margin buffer:

If input costs increase by 15 per cent across freight-exposed lines, does the client have the pricing power to pass that through to customers, and the contract terms that allow them to do it in time?

The RBA's liaison data from February 2026 shows that many consumer-facing firms found it difficult to pass on cost increases during periods of weak demand, only recovering margin capacity when conditions strengthened. An SME with thin margins, price-sensitive customers, and fixed-price contracts has no buffer. That is a cash flow risk. The question is not whether costs will rise. It is whether the business model can absorb the timing gap between cost increases and price recovery.

If a client scores high exposure across all three channels, the conversation needs to move from assessment to action. That action framework is the subject of the third part of this series.

Problems first, platforms second, and right now, the problem is a slow-moving cost shock that most SME clients have not yet mapped against their own financials.

What's coming in this series

This article has established the mechanism. The next two pieces make it actionable.

Part 2: "Which of your clients are in the blast radius?" focuses on the specific industries where Middle East exposure is acute, where it is moderate, and where some clients may actually find unexpected opportunity. Not all firms face the same risk. The mistake most accounting practices are making right now is treating geopolitical exposure as background noise that affects everyone equally. It doesn't. Part 2 gives you an industry-by-industry risk map and a diagnostic framework you can use in your next round of client conversations.

Part 3: "The call your clients are about to make" is about what you do with that map. It covers the specific advisory conversation that needs to happen now, before the escalation, not after, and the three concrete deliverables you can produce for at-risk clients in the next thirty days. This is where the accountant's role shifts from compliance function to trusted strategic adviser.

Together, the three parts form a complete toolkit: the mechanism, the map, and the response.

The accountant’s real job right now

The Brisbane building supplies owner did not need a geopolitical analyst. They needed their accountant to understand the transmission mechanism well enough to explain it, and to start asking the right questions before the next invoice arrived.

Geographic distance has never been the same thing as economic insulation. The firms that understand this now will arrive at the next disruption with plans in place. The firms that don't will arrive with questions, and by then, the questions will cost them.

Andrew Cooke is the founder of Growth & Profit Solutions AI (GPS-AI).

Make Accountants Daily a preferred news source on Google.