Transitional Payday Super rules could cause SG problems for many employers

BusinessJason Hurst, Accurium's technical superannuation adviser, outlines complex transitional rules related to Payday Super which could expose employers to unexpected outcomes.

Most practitioners and many employers will be familiar with the new Payday super timing rules which apply from 1 July 2026 and require superannuation guarantee (SG) contributions to be in an employee’s superannuation fund within 7 business days after the payment of salary or wages.

However, there are also some important changes to the late contribution rules and complex transitional rules that will apply from 1 July 2026 to 28 July 2026 which could expose employers to unexpected outcomes.

The first 28 days of July 2026 will be a time where many employers will be juggling SG requirements from the June 2026 quarter and the new Payday super requirements. This will be a challenging period for cashflow and due to the way contributions are allocated during this transitional period, employers may end up with unexpected SG shortfalls.

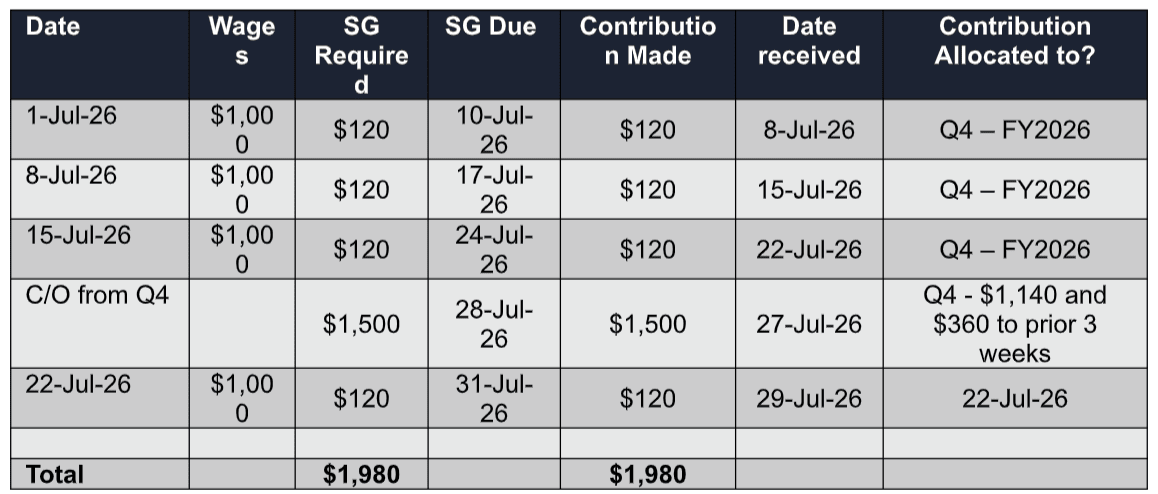

Let’s consider an example of a business which employs Gary. Over the month of July 2026 Gary has four paydays where he receives $1,000 per week. He is also owed $1,500 in SG from the June 2026 quarter, which is due by 28 July 2026.

Looking at table 1 it appears at first glance that Gary’s employer has made all contributions on time. However, under the transitional rules, contributions made between 1 July and 28 July 2026 are first taken to clear any outstanding amounts from the prior quarter.

Because Gary’s June 2026 quarter SG amount of $1,500 is still outstanding (but not late!) until after the first three payday due dates, the three initial $120 contributions are allocated to reducing the shortfall from the prior quarter. This means that the SG for the first three pays in July would not be considered paid until 27 July 2026 resulting in three late payments.

Table 1 – July 2026

While cashflow may be a challenge for many businesses at this time, employers should consider whether they could commence making SG contributions on a payday cycle earlier than 1 July 2026. If not, employers should look at whether they are in a position to pay their June 2026 quarter SG amounts prior to their first payday in July so that they can start 1 July 2026 with a clean slate and focus on the new payday due dates.

Another important change is that it will no longer be possible for employers to choose to allocate a late contribution to the period that it was received by the employee’s super fund. From 1 July 2026 employer contributions will be automatically allocated to the pay period with the oldest outstanding SG liability. For example, if Gary’s employer was to miss a weekly SG contribution in August 2026 and not pick this up for some time each subsequent weekly super contribution would be allocated to the prior week’s SG liability and there would be a shortfall for each subsequent week until the issue is picked up, and rectification steps are undertaken.

This makes it critical that employers have robust processes in place to minimise errors and, if they do occur, to ensure they are spotted quickly and rectified as soon as possible. Now is the time to contact your software providers to understand what support and enhancements they are planning to help track Payday super liabilities.

From 1 July 2026, SG administration penalties may be as high as 60 per cent of the shortfall and notional interest amount (up from $20 per employee per period) however these penalties may be remitted to as low as zero where employers with a good history promptly fix issues and self-disclose to the ATO.

Make Accountants Daily a preferred news source on Google.